A primer illustrating how options can be used to generate consistent risk-adjusted returns across market conditions

It is the job of a trader to generate consistent risk-adjusted returns no matter what the market regime. This is often hardest in a sideways market – a market lacking in any distinct trends, where price action oscillates within a largely horizontal range. However, more experienced traders can find opportunity in such conditions, especially those who incorporate options strategies for yield enhancement or volatility exposure.

Understanding how to use options effectively is key in managing this new crypto winter. Below is an initial exploration of market characteristics and key considerations around a number of potential options strategies for this environment.

Sideways markets are when the price of a security trades within a horizontal channel, without displaying any definitive bullish or bearish trends. Usually, in such a market, prices are range-bound between very strong support and resistance levels. Volume may be falling or flat; and can also be accompanied by declining realised volatility.

Many traders, especially those who rely on momentum or trend-following strategies, would agree that such markets can be difficult to trade as there is uncertainty around the direction and timing of the next breakout. One potential solution for the experienced trader is to consider using option trading strategies.

Options strategies have a few key advantages: flexibility and non-linearity. By being able to pick strikes and tenors, traders can be more precise about speculating on when, how much, and how quickly the underlying asset will move. Also, by developing an understanding of greeks and options theory, traders can ascertain if the non-linear payoff profile works in their favour and either hedge their position or improve profitability in quieter periods. Effective risk management should always be a key consideration in building and implementing such strategies.

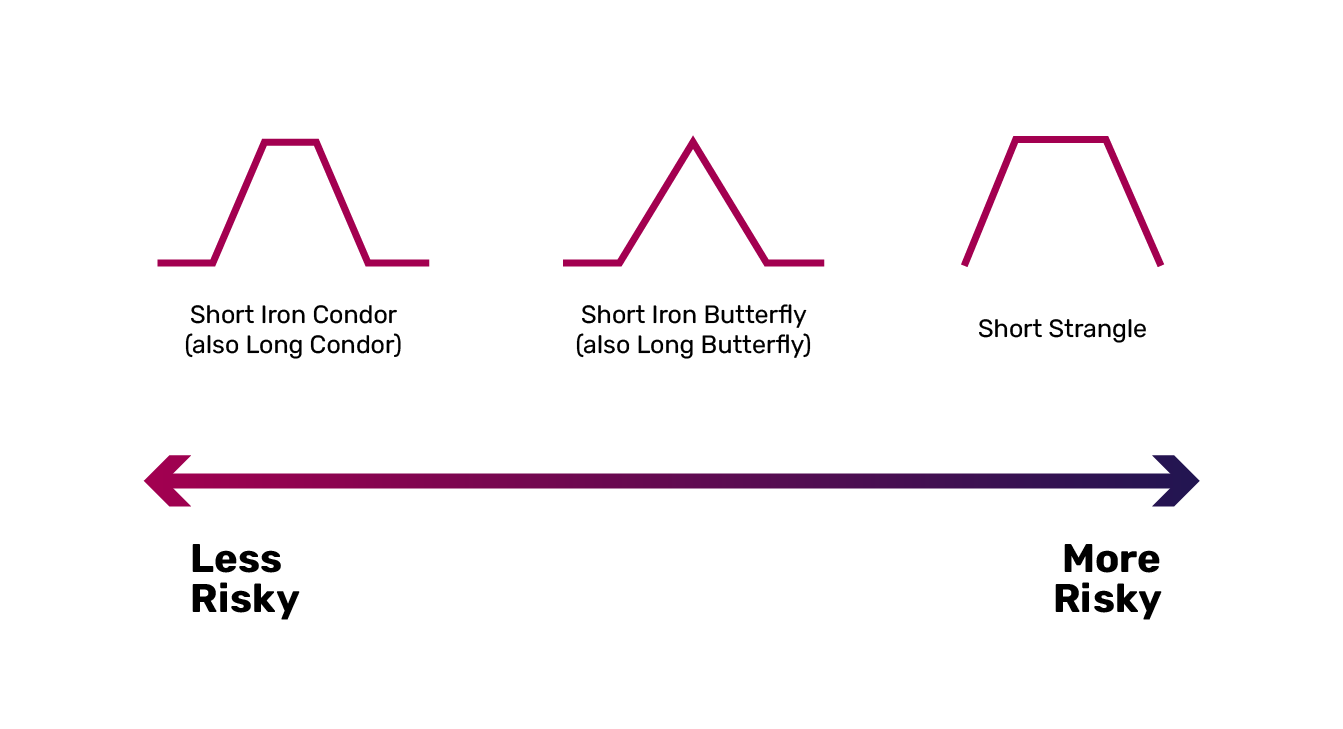

In sideways markets, there are a number of options structures that aim to sell premium (sell options worth more than the ones you buy i.e. net selling options) and thus increase profitability. These are essentially yield enhancement structures like: Short Iron Condors, Short Iron Butterflies and Short Strangles.

A way to grind out modest wins and enhance profitability over time without getting hit big time. Essentially by selling a Short iron Condor the trader is hoping trading will remain in the narrow band so all contracts are OTM on expiry, meaning they keep 100% of the premium.

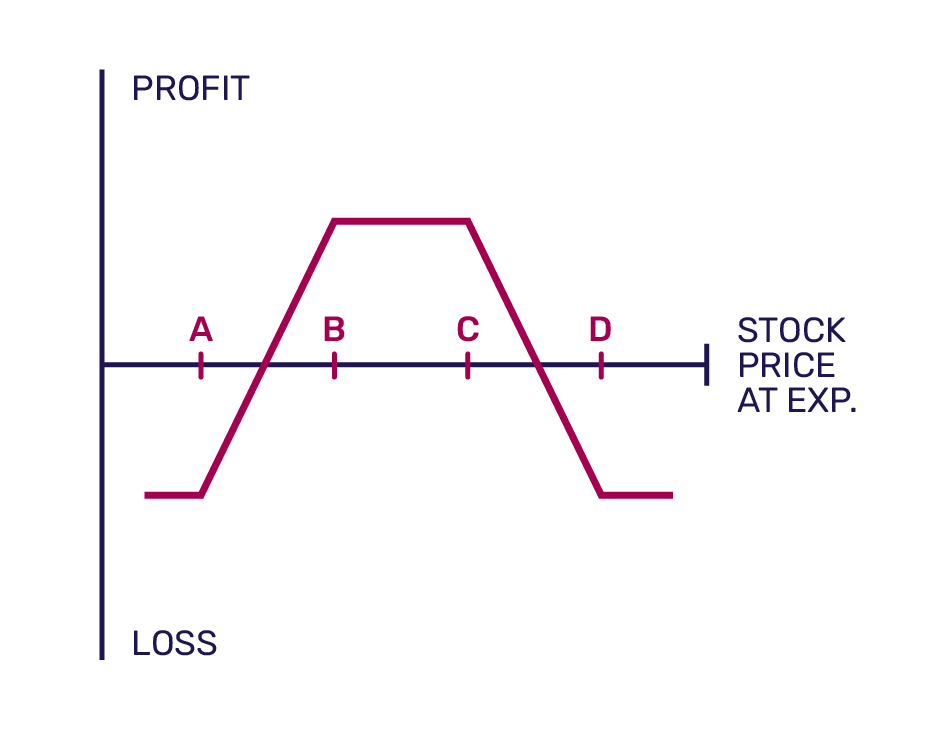

Assuming the underlying is between B and C in price, the setup is as follows: sell one out-the-money [OTM] put spread (sell put option B, buy put option A) and sell one OTM call spread (sell call option C, buy call option D). Usually, the distance between strikes C and D matches the distance between B and A. The wider the distance between B and C, the wider the band where the trade is profitable but the tradeoff is that the potential profit is lower.

At initiation, the trader will receive a net credit into the account and will keep all of this if the underlying stays between B and C when the options expire. There are two break-evens, strike B minus the credit received and strike C plus the credit received. The risk on this structure is the underlying ends below A or above D at expiry, then the max loss will be the difference between the strikes D and C (or B and A), less the credit initially received.

A similar payoff profile can be achieved through a Long Call Condor (buy one in-the-money [ITM] call spread, sell one OTM call spread) or Long Put Condor (buy one ITM put spread, sell one OTM put spread) but these strategies require you to pay premium. Investors tend to prefer the Short Iron Condor due to the net credit received initially, but should be conscious that the Long Condor structures are better from a margin perspective.

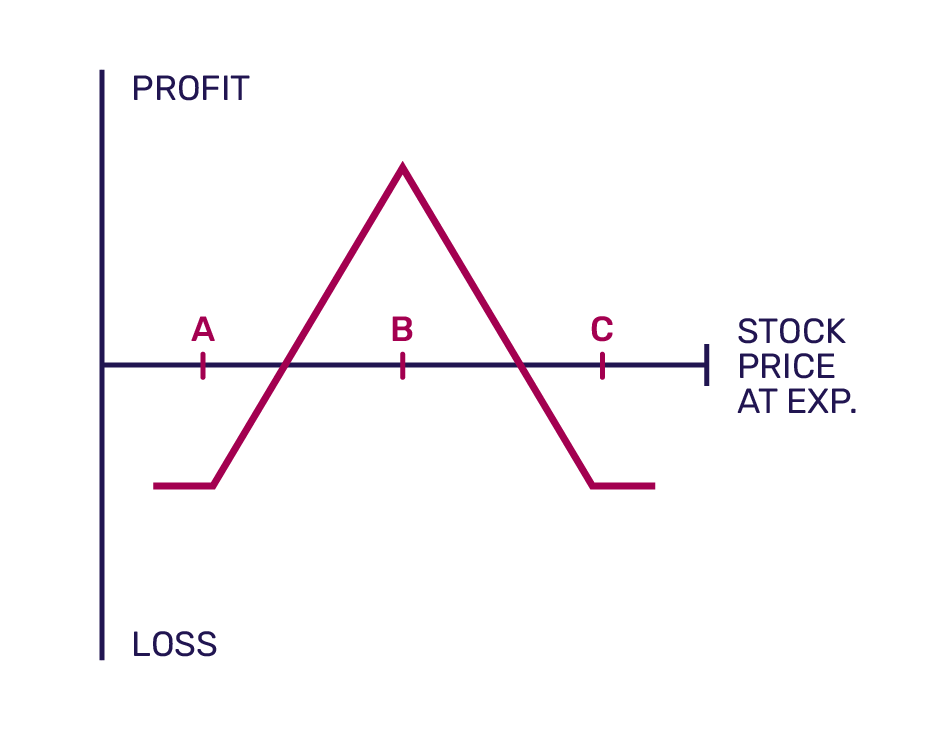

Iron butterflies are designed to provide traders with steady income while limiting risk. The expectation is that price volatility will remain within a narrow band and the nearer to the middle strike price the underlying closes at expiration, the higher the profit.

This structure is set up as follows: sell put spread (sell put option B, buy put option A), sell call spread (sell call option B, buy call option A). It is essentially a Short Iron Condor from above, where strike B = strike C. Thus, this structure also receives a net credit at initiation.

The best case scenario is that the underlying is exactly at B at option expiry, and then all options expire worthless and the trader keeps all of the initial credit. However, this is extremely unlikely and so expect either the call or put option at strike B to expire ITM. The breakevens are Strike B plus / minus the net credit received.

Bullish investors would choose strike B to be above the underlying price at initiation and the opposite would hold for investors with a bearish view. Investors also have the choice of replicating a similar payoff profile through a Long Call Butterfly or Long Put Butterfly, with similar considerations to the Condor / Iron Condor example above.

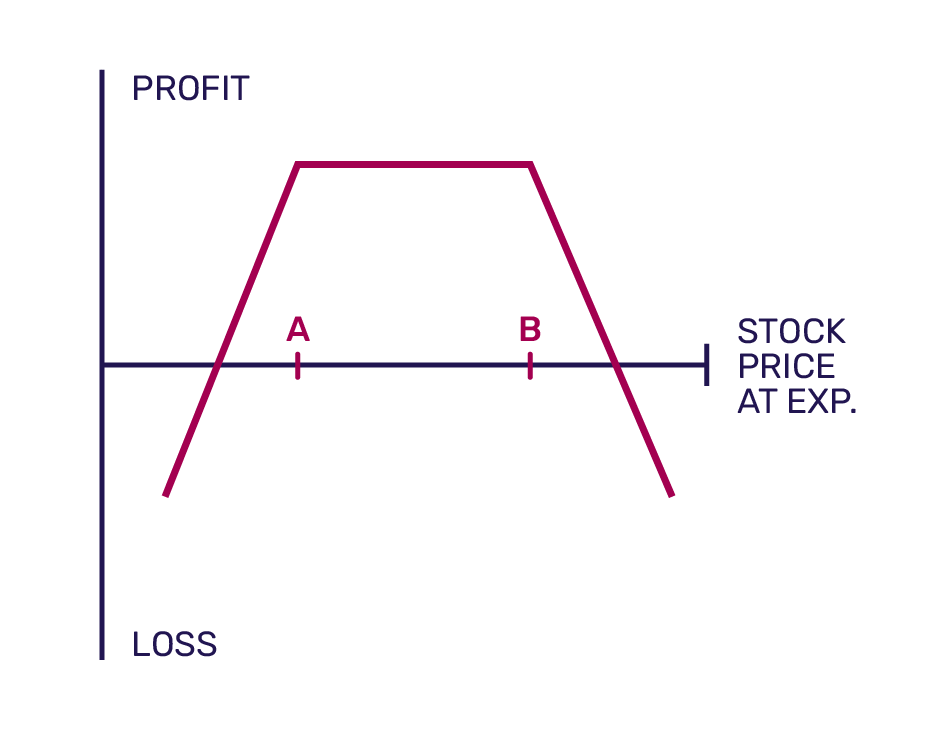

If you have strong conviction that the underlying will stay within A and B for some time period, then an aggressive options strategy to profit from this is the Short Strangle. Here, the setup is: sell OTM put option at Strike A, sell OTM call option at Strike B (assuming the underlying is between A and B).

You receive a significant net credit at initiation from selling two options, but are exposed to unlimited loss to the upside, and substantial downside risk (if the underlying goes to 0). The breakeven points are A minus the net credit received and B plus the net credit received.

This structure also gives you Short exposure to Implied Volatility (i.e the position is Short Vega). Hence, savvy investors can time the market by selling strangles when they feel there has been an unjustified increase in Implied Volatility. As sideways markets are often accompanied by declining realised and implied volatility, this strategy can be very profitable if executed and managed appropriately.

In sideways markets, the front-end of the volatility term structure (near-dated options) usually falls by more than the back-end (far-dated expiry options). This is due to low realised volatility in range-bound markets and options traders lowering Implied Volatility expectations for the near-term whilst still being neutral on longer dated volatility expectations - as who knows what will happen!

To profit from this phenomenon, traders can use variants of a Long Calendar Spread in different ratios, Straddle / Strangle Swaps and bespoke structures that replicate Iron Condor like payoffs across expiries.

With the stock usually at price A, this structure is usually set up as follows: sell call option strike A for a near expiry, buy call option strike A at a later expiry. By symmetry, the structure can also be put on using put options.

If done 1:1, this structure is short Gamma, collecting Theta, long Vega - and costs money at initiation as the back-dated option is worth more. This means as long as there is minimal movement in the underlying, you collect Theta every day - this is because the shorter dated option loses value more than the longer dated option every day. The best case scenario is that the underlying is exactly at A when the near dated option expires (so it expires worth 0). The potential profit is limited to the premium received for the back-date option, less the cost of buying back the near-dated option minus the net debit paid at initiation.

The trade can also be done Vega flat - this is a lot more aggressive as more of the front-dated options need to be sold for every one back-dated option bought.

This is essentially a Long Calendar spread with multiple options in each expiry. You sell a near-dated Straddle / Strangle and buy a further-dated Straddle / Strangle. Various combinations of strikes can be chosen to optimise the overall greek profile of the structure and choose break-even points appropriately. Some structures can also be long Gamma, long Vega and collecting Theta! Finally, as Straddles / Strangles are mostly relatively delta-neutral structures, this has the advantage of not needing to trade much Delta as spot varies within its range.

A trader familiar with options theory can find opportunity in any market regime, even in a sideways market where trends are hard to determine.

The flexibility of options, especially bespoke OTC options strategies, is crucial for generating profits during periods of stagnant price action in the underlying asset. The convex payoff profile can also work for you if you know how to harness it.

Bottom line: understanding and incorporating options will enable you to trade with confidence in any market environment. ■

This piece is solely for discussion/information purposes only and does not constitute an offer or firm commitment of any kind to provide any investment opportunity, product or return.

Investments involve risk, and this document does not purport to identify all (if any) of the risk factors associated with any exposure to the proposed product or instruments, assets, or currencies referenced therein. There is no guarantee of any returns or yields. The value of investments may fall as well as rise and any investment may result in loss which may be significant.

Product are available for investors who are either professional, accredited or sophisticated investors, and any such investor will be investing on the basis of its own assessment of its financial ability and willingness to accept the risks inherent in the product or instruments, assets or currencies referenced therein. The product is not available for retail investors.

No representation, warranty, assurance or undertaking (express or implied) is given (and can therefore not be relied upon as such), and no responsibility or liability is or will be accepted by B2C2 Ltd or any of its affiliates or any of its or their respective officers, employees or agents as to the adequacy, accuracy, completeness or reasonableness of the information, statements and opinions expressed in this document.

Any opinions expressed in this document do not constitute legal, tax or investment advice and can therefore not be relied upon as such. Please consult your own legal and tax advisers concerning such matters.

B2C2 Ltd is registered in England and Wales under company number 07995888 with its registered office at 86-90 Paul Street, London, EC2A 4NE. B2C2 Ltd is the parent company of the B2C2 group of companies. Products may be provided by different members of the B2C2 group of companies, depending on the jurisdiction of the client and the regulatory status of the product and/or B2C2 group member.

B2C2 is a registered trademark.

B2C2 is a global leader in institutional liquidity for digital assets. Founded in 2015, we are trusted by blue chip hedge funds, institutional managers, brokers, crypto exchanges, and crypto foundations. We provide deep, reliable liquidity and pricing in crypto, delivering seamless execution 24/7/365. Majority owned and backed by Japanese financial conglomerate, SBI, B2C2 Ltd is headquartered in the UK, with offices in the US, Japan, Singapore, France and Luxembourg.

B2C2 Ltd is registered in England and Wales under company number 07995888 with its registered office at 41 Lothbury, London, EC2R 7HF. B2C2 Ltd is the parent company of the B2C2 group of companies. Products may be provided by different members of the B2C2 group of companies, depending on the jurisdiction of the client and the regulatory status of the product and/or B2C2 group member. B2C2 is a registered trademark.

For institutional and professional investors only. For information purposes only. See full risk disclosures here.

Sign up to our news alerts to receive insights into the crypto market.

B2C2 does not transact with or provide any service to any retail investor or consumer. By subscribing to our content, you represent that you are not a retail investor or consumer. Please refer to our disclaimer for further information.