Crypto prices have been rather sideways over the past week, implying that the market priced in a hawkish Fed before it was confirmed. Since then BTCUSD squeezed a little higher into the event, and again over the weekend, but both times the rally petered out before $39k, and ultimately the week turned out range bound in falling volumes. ETH has been a similar story, with $2,700 resistance for now. Of the coins we trade, only LUNA has made fresh lows since last Wednesday, reaching $43.50 today.

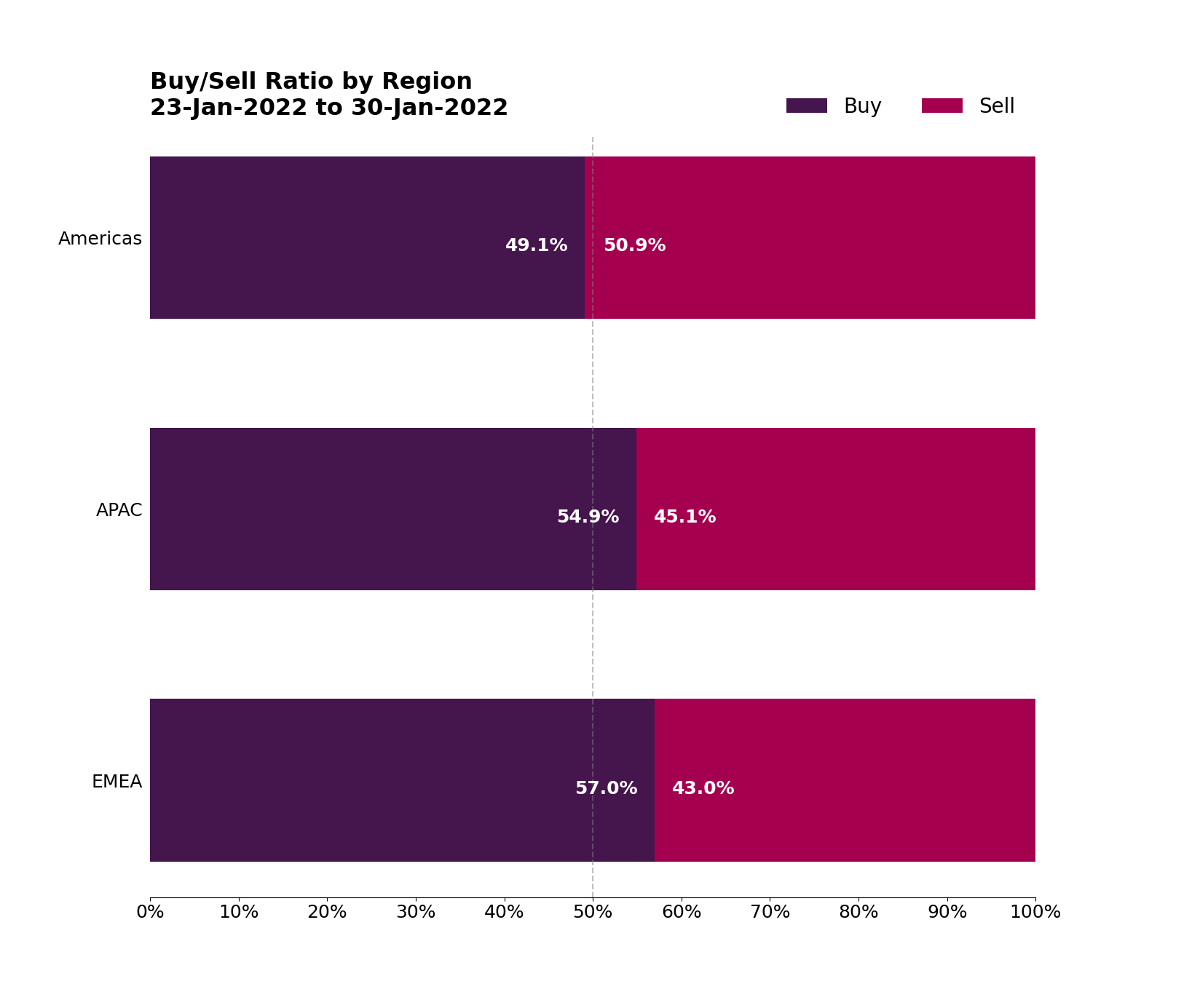

Our flow data shows that crypto exchanges and banks have been the biggest buyers, with family offices primarily sellers. By region we see the Americas split evenly, with APAC and EMEA biased towards buy flow. By coins, we have seen strong selling in DOT and better buying in MATIC, XRP, XLM, XTZ and UNI.

Futures market forward bias has remained fairly stable, with annualised basis at 2.5-3.0% in 1-month and 5-6% in 3-month on the more liquid exchanges. While we have detected no significant change in USD supply/demand on the OTC side, we have noticed an uptick in demand to borrow BTC, resulting in a slightly higher depo curve there. This is mainly to facilitate reverse basis trades, given that basis across the term structure is firmly lower than the OTC lending market.

In the options market, vols remained bid until the end of last week, as did put skew. In fact, the put skew held up better than vols towards the end of the week, with longer dated risk reversals also catching a bid. BTC 1-month ATM vol has drifted lower from 72 to 65 vol since the Fed, while put skew has actually moved higher. March 25 delta BTC riskies now 6-7 vols for puts which is a high since May/June last year, when crypto suffered from serious risk aversion as the price flirted with $30k support.

This week we have US payrolls which could be an interesting number. Consensus expectation is for +175k to +200k jobs, but variance is high, as January was Omicron-afflicted, and some analysts are calling for a negative number. However, it will probably be academic anyway: the Fed views the underlying labour market as very strong, so is likely to look through volatility in the January number itself. Otherwise we have BoE who are expected to raise, and ECB who are not, on Thursday. The ECB is expecting inflation to have already peaked though, so Wednesday’s release of EU CPI data will be keenly watched as an indicator for risks to EU rates.

B2C2 is a global leader in institutional liquidity for digital assets. Founded in 2015, we are trusted by blue chip hedge funds, institutional managers, brokers, crypto exchanges, and crypto foundations. We provide deep, reliable liquidity and pricing in crypto, delivering seamless execution 24/7/365. Majority owned and backed by Japanese financial conglomerate, SBI, B2C2 Ltd is headquartered in the UK, with offices in the US, Japan, Singapore, France and Luxembourg.

B2C2 Ltd is registered in England and Wales under company number 07995888 with its registered office at 86-90 Paul Street, London, EC2A 4NE. B2C2 Ltd is the parent company of the B2C2 group of companies. Products may be provided by different members of the B2C2 group of companies, depending on the jurisdiction of the client and the regulatory status of the product and/or B2C2 group member. B2C2 is a registered trademark.

Sign up to our news alerts to receive our regular newsletter and institutional insights into the crypto market direct to your inbox.

B2C2 does not transact with or provide any service to any retail investor or consumer. By subscribing to our content, you represent that you are not a retail investor or consumer. Please refer to our disclaimer for further information.